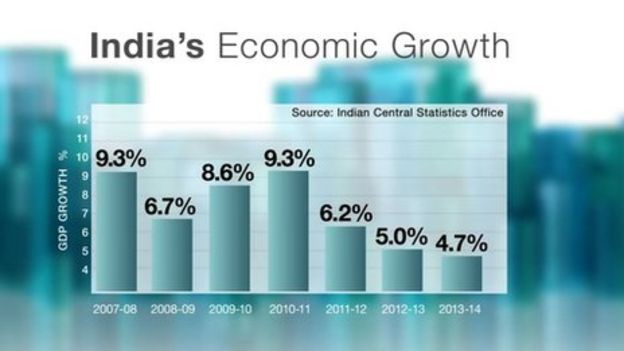

India’s gross domestic product (GDP) grew 7.6 per cent in 2015-16, powered by a rebound in farm output, and an improvement in electricity generation and mining production in the fourth quarter of the fiscal. Economic growth was estimated at 7.2 per cent in 2014-15.

India’s gross domestic product (GDP) grew 7.6 per cent in 2015-16, powered by a rebound in farm output, and an improvement in electricity generation and mining production in the fourth quarter of the fiscal. Economic growth was estimated at 7.2 per cent in 2014-15.The growth numbers for the last fiscal, which reinforces India’s position as the world’s fastest-growing large economy, came on the back of a strong 7.9 per cent growth in the last quarter of the fiscal.

The robust headline number, despite faltering private investment, weak capital goods growth and shrinking exports, has reinforced expectations that the RBI would keep its policy rate on hold at its next quarterly review next Tuesday. The central bank has already cut its policy repo rate by 150 basis points since January 2015, reducing it to 6.5 per cent — the lowest level in more than five years.

The strong 7.9 per cent growth in the fourth quarter comes at a time when China has reported a 6.7 per cent in the March quarter — its slowest growth in about seven years.

According to data released by the Central Statistics Office (CSO), the farm sector grew by 2.3 per cent from a year ago compared with a 1.0 per cent contraction in the December quarter. Mining grew 8.6 per cent in the March quarter, up from 7.1 per cent in the previous quarter. Electricity, water and gas production growth surged to 9.3 per cent from 5.6 per cent in the December quarter.

The CSO, in a statement, said that it has revised the GDP data for the first three quarters released earlier from 7.6 per cent, 7.7 per cent and 7.3 per cent to 7.5 per cent, 7.6 per cent and 7.2 per cent, respectively.

Also, the growth of in the “agriculture, forestry and fishing” sector was revised upwards to 1.2 per cent in 2015-16 as against 1.1 per cent in the advance estimates for the same period. “The upward revision is on account of the use of third advance estimates of crop production released by the Ministry of Agriculture,” it said.

The manufacturing sector’s growth was also revised downward to 9.3 per cent as against the growth rate of 9.5 per cent estimated earlier due to lower print of industrial output than estimated earlier. “The IIP of manufacturing registered a growth rate of 2 per cent during the whole year of 2015-16, as against the growth rate of 3.9 per cent used for compiling Advance Estimates. Due to this change, the advance estimate growth of ‘manufacturing’ sector has been revised downwards to 9.3 per cent,” it added.

Growth of trade, hotels, transport, communication services has been revised downward to 9 per cent against 9.5 per cent estimated earlier, while financial, insurance and real estate sector grew at 10.3 per cent, same as projected earlier.

Upasna Bhardwaj, Economist, Kotak Mahindra Bank, said that private consumption has been holding up, mirroring some of the progress in high frequency data such as auto sales and the improving prospects of adequate monsoons.

“Another reason for the pickup in private consumption could be attributed to the heavy dividend payouts by corporates rather than increasing investment spending. Overall, the continued weakness in capital goods production and lack of capacity addition continues to remain a drag on growth. Going forward, better monsoons and seventh pay commission payouts are likely to remain supportive of consumption. However, private capex will likely remain the missing link for a few more quarters with growth continuing to be heavily reliant on government spending. We, therefore, see a gradual uptick in growth next year,” she said.

The Economic Survey had projected a wide band of 7-7.75 per cent growth in 2016-17, boosted by normal monsoon projection. It had, however, cautioned that with the global slowdown likely to persist, chances of India’s growth rate in 2016-17 increasing significantly beyond 2015-16 levels were not very high.

The RBI, too, in its April monetary policy review, said a number of factors could impinge upon the growth outlook for the current fiscal such as slow investment recovery amid balance sheet adjustments of companies, weak revival of private investment demand and tepid external demand.

No comments:

Post a Comment